For suppliers considering entry into the nuclear market, the key question is not simply whether the market is improving, but whether conditions justify investment. This analysis highlights the key signals and capabilities that suppliers should assess before committing to the nuclear market.

Prospective suppliers to the nuclear power industry – from reactor OEMs and fuel suppliers to EPCs – are considering if and when commercial nuclear could be a growth platform. After years of natural gas price and Fukushima driven safety concerns, the last year has brought a flurry of positive supply and demand signposts. But are they enough to drive the industry forward, and what risks would a supplier face by investing now?

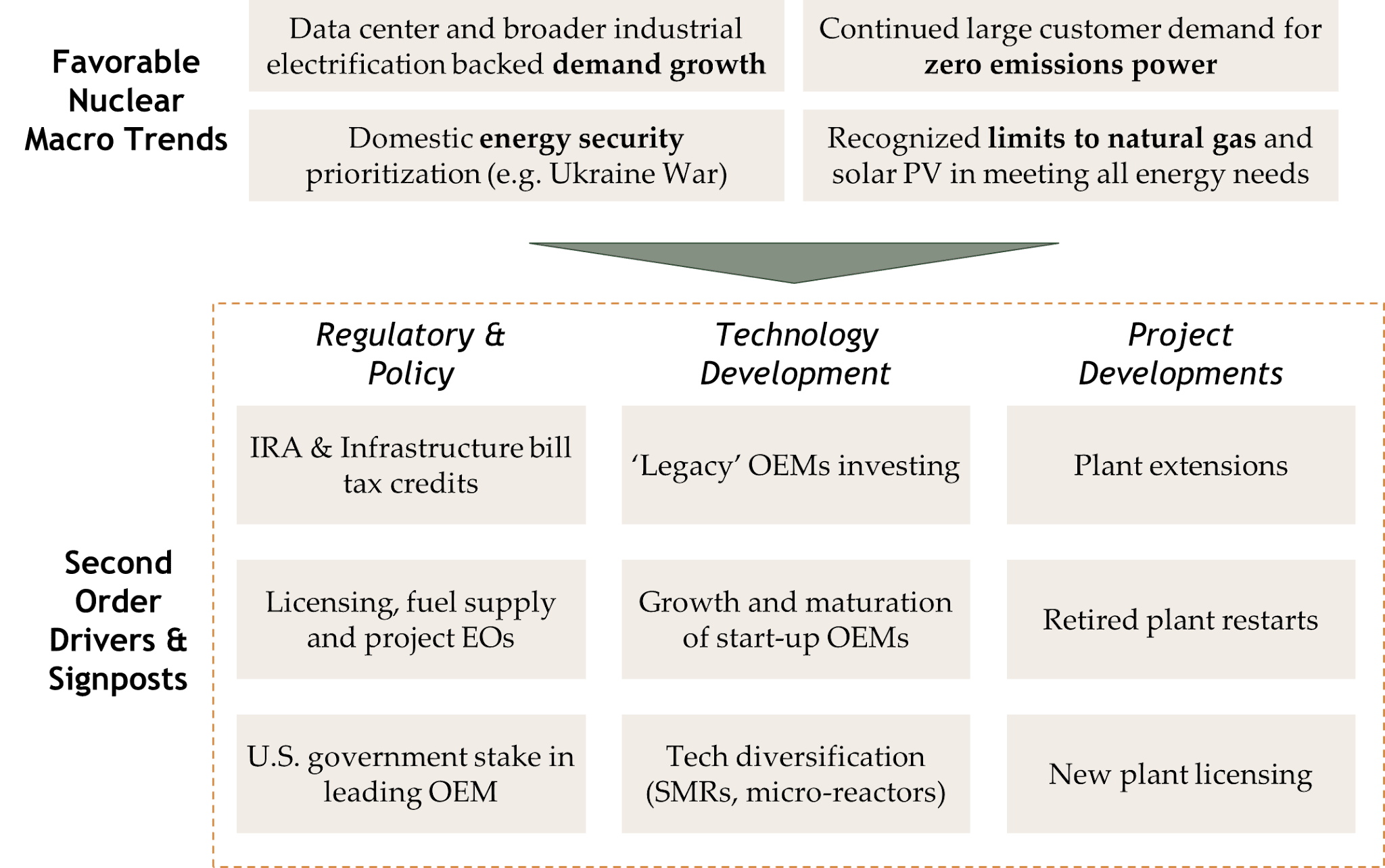

Looking back further, the seeds for some of these stimulants were planted in the wake of the last round of nuclear enthusiasm, starting in 2005 and commonly referred to as the Nuclear Renaissance. These include the growth in new reactor product development by both legacy incumbents (e.g. GE Vernova Hitachi) and first time reactor developers (e.g. Holtec and NuScale) to the 2022 Inflation Reduction Act’s (IRA) new Clean Electricity production and investment tax credits (PTC and ITC). While nuclear power has benefited from bipartisan support in the U.S., Trump 2.0 has injected substantial regulatory and financial support through a mix of Executive Orders and agency action including a goal of quadrupling nuclear capacity by 2050.

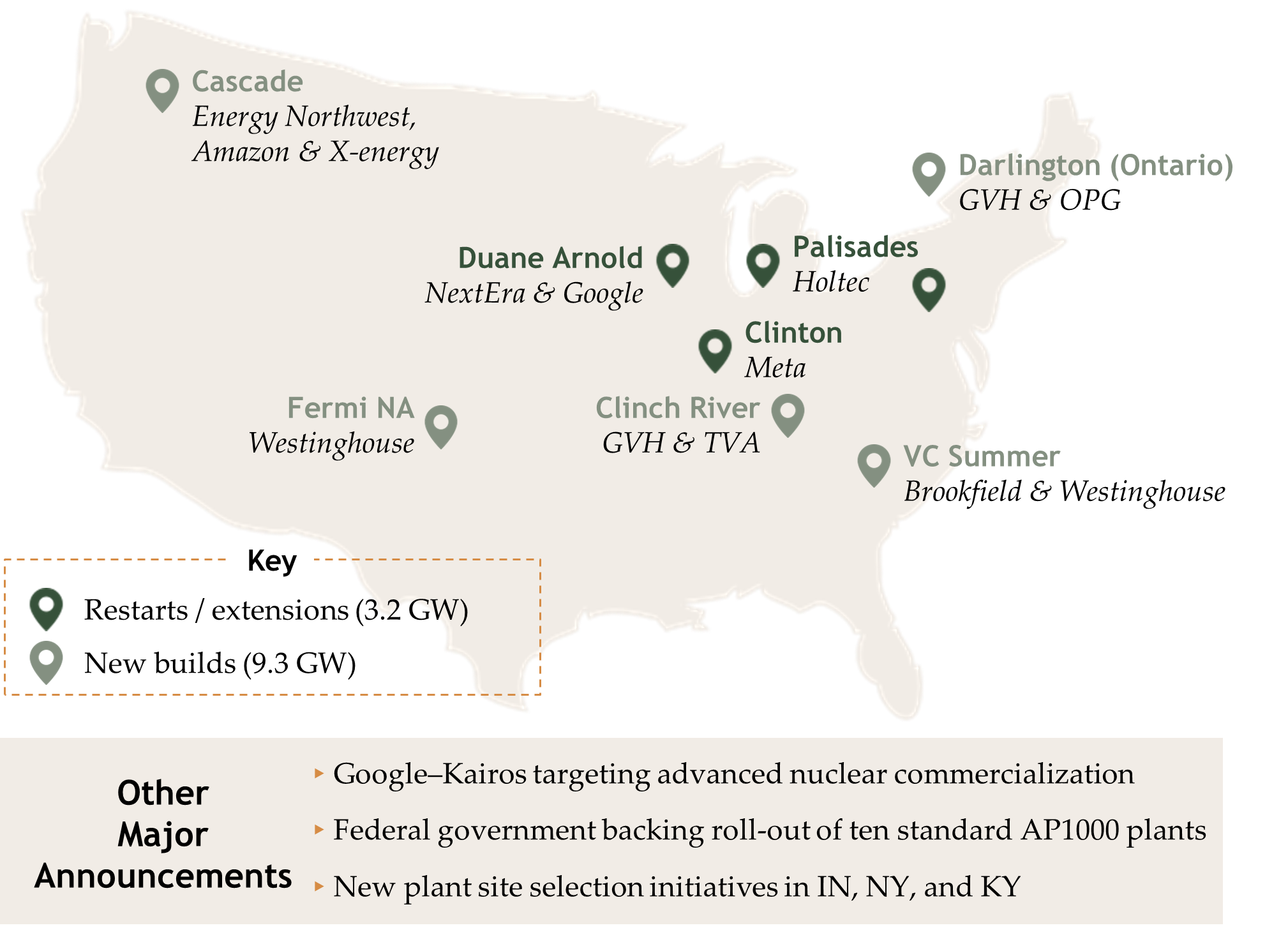

On the energy buyer side, leading data center hyperscalers have announced plans to restart existing plants as well as new projects. Moreover, the Executive Branch announced financial guarantees to Westinghouse and Cameco to deploy ten Westinghouse AP1000 units, setting a demand baseline that will help mobilize the supply chain and accelerate project execution lessons learned. Taken together, these announcements represent over 10 GW of potential nuclear power capacity expansion in the U.S. – equivalent to approximately 10% of the current installed base. While these announcements are material, they do not yet constitute a structural inflection in national capacity deployment.

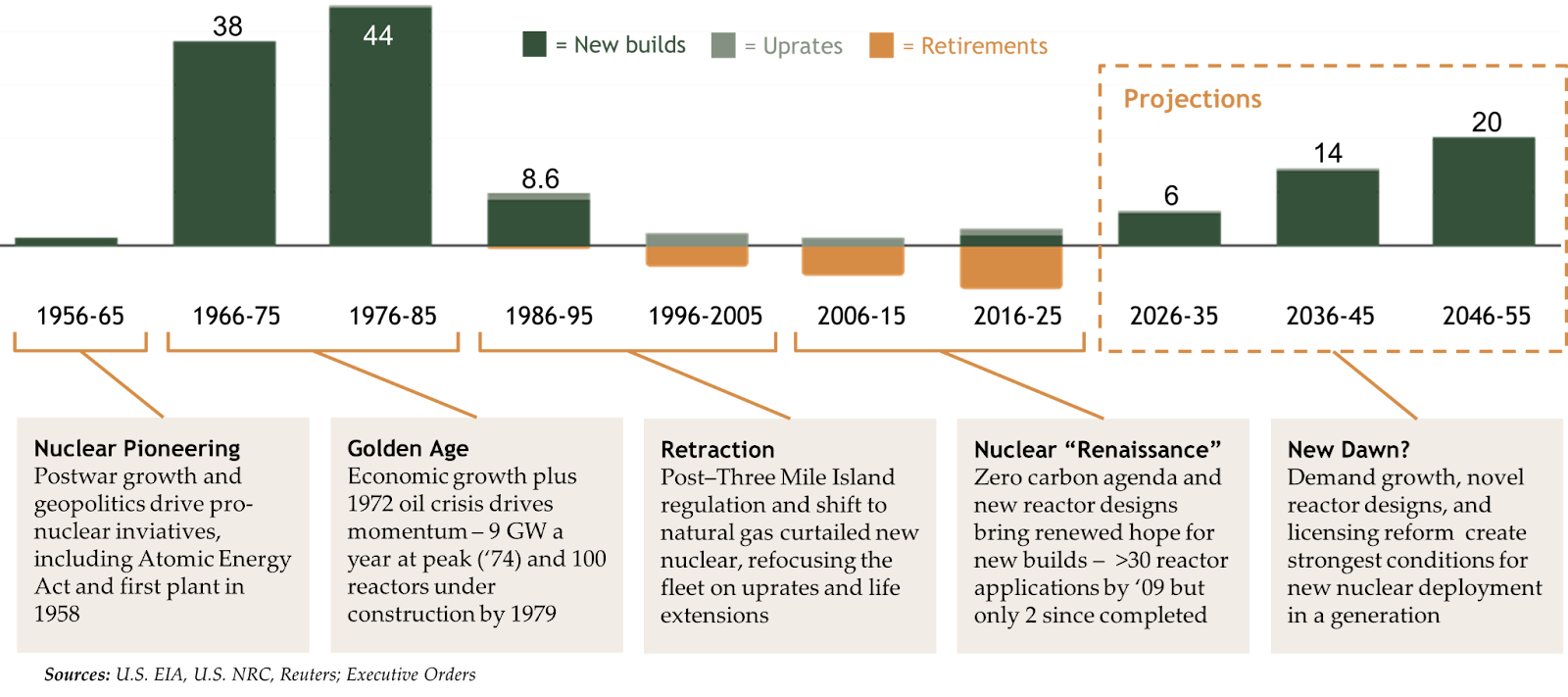

Owner announcements, executive orders, and capital flows, however, are far from sufficient to guarantee demand materialization in the next decade, much less a nuclear renaissance. While such capacity additions would reverse the net reductions over the last 30 years, they would constitute only a marginal nuclear power contribution to electricity demand growth. Some investors and energy planners, however, are extrapolating the favorable nuclear regulatory, policy, and technology trends into step-change expectations in nuclear power capacity longer term, as illustrated in Figure 3.

While expected capacity additions over the next few decades are far lower than the peak of the 1970s, the industry challenges remain substantial. The industry's past, characterized by unfulfilled expectations, serves as a stark reminder. For instance, following the submission of 31 new build license applications in the U.S. between 2007 and 2009, only Southern Company’s Vogtle 3&4 ultimately reached completion. Enthusiasts, however, claim “this time is different”, a sentiment that likely reminds seasoned executives of past, overhyped market trends.

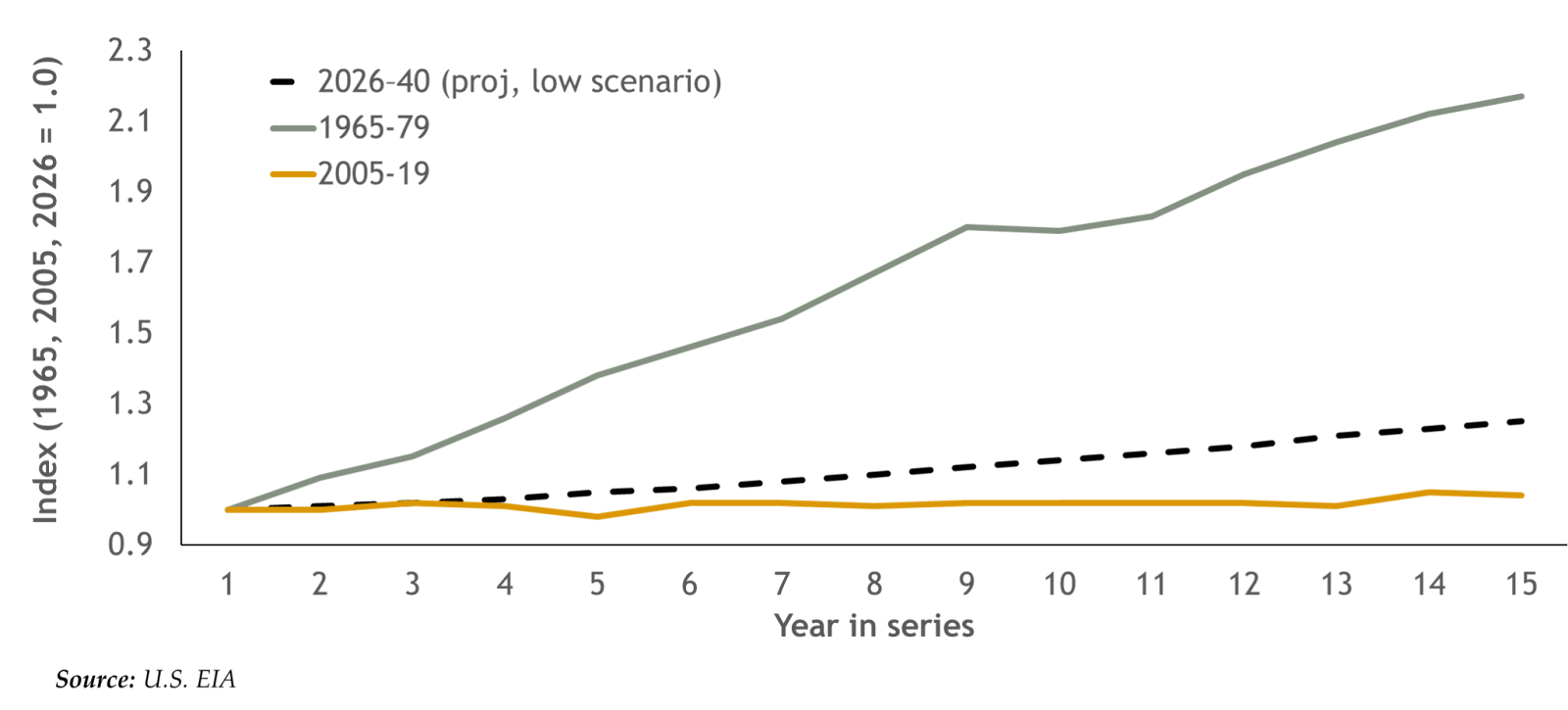

The central question is whether today’s demand environment fundamentally alters the commercial calculus for suppliers. In some regards, current dynamics indeed differ from the above referenced Nuclear Renaissance. Crucially, unlike the 2005–15 period when consumer electricity demand was essentially stagnant, current growth expectations—driven by data center construction and a broader increase in electrification—are unlike anything seen since the last major nuclear build cycles in the 1970s. As Figure 4 demonstrates, while still far from the 1960-70s pace of growth, even conservative electricity demand growth projections surpass expectations at the time of the false start Nuclear Renaissance.

Just as important as the scale of the demand potential is its alignment to both commercial interests of a concentrated set of customers as well as national interests. Because a handful of sophisticated tech companies rely on power supply expansion (preferably zero emissions), demand certainty and proactive engagement is more easily secured than if demand growth were diffused across uncoordinated commercial and residential interests. Unlike previous nuclear new build waves, some customers are engaging not only with project owners but also reactor suppliers, financing entities, and regulators. Moreover, the link between data centers and the geopolitical race for AI leadership brings executive branch support. Specifically, the Trump administration has committed to licensing acceleration and expanded optionality for DOE licensing through its May 2025 Executive Orders.

Lastly, new business models are emerging which promise to partially mitigate the financing and project risks that loom over the nuclear new build environment. For example, a growing list of prospective development companies leverage private equity and venture capital funding to bridge financing gaps. Some also include engineering and project management leaders from previous new nuclear projects from which to apply cross project learnings, increase efficiencies, and reduce project execution rework.

Despite the concurrence of supply and demand spurs in the last couple years, a wide mix of keys are still needed to unlock the potential for a 20+ GW decade of nuclear capacity expansion. Nuclear new build component and/or service suppliers face a complex web of interdependent and highly uncertain market signals to determine if, when, and how aggressively to invest in resources, equipment, and commercial initiatives. Suppliers' nuclear go-to-market strategy planning should be guided by five key assessments, three external and two internal:

How these dynamics translate into real supplier decisions is illustrated in two case studies of Solestiss-led projects – one for an incumbent supplier and the other for a potential new entrant.

Buoyed by growing certainty for the nuclear installed base, a major commercial nuclear services provider sought growth through a bundled outage-services offering. Solestiss led a review of market conditions, internal capabilities, and execution readiness to recommend a go / no-go strategy. Solestiss re-baselined the addressable market based on contractual and regulatory constraints, voice of customer interviews, and its own perspectives. Furthermore, Solestiss led internal stakeholder interviews to assess the supplier’s offering competitiveness.

Solestiss determined that customer demand was limited and that internal execution systems would require further maturation to meet customer performance requirements. The supplier deferred broad market launch and instead focused on strengthening execution systems and continuing demand validation. This risk-informed decision helped leadership avoid premature expansion while positioning the organization for stronger future entry. The engagement underscored that sound market strategy must consider both internal and external readiness.

After decades in the naval nuclear market and drawn by commercial nuclear demand growth potential, a leading supplier saw growth potential in commercial nuclear power. While the company recognized that this market requires distinct regulatory, contractual, and supply chain dynamics, management needed objective guidance on where it could compete effectively without overextending its capabilities or assuming disproportionate risk.

Solestiss led a comprehensive target market prioritization based on demand timing, client internal capabilities, and supply chain positioning. Solestiss’ recommended strategy and execution plan identified priority initial customers and commercial opportunities consistent with the client’s manufacturing footprint and organizational readiness. The engagement addressed practical questions facing many suppliers: not simply whether opportunity exists, but where to engage, at what pace, and under what conditions. The result was a disciplined go-to-market strategy that enabled leadership to move forward deliberately rather than speculatively.

The path to established nuclear energy supply and demand will be more protracted and volatile than other energy sub-sectors, let alone non-energy markets where some participants are active. For certain suppliers without a nuclear focus, such as EPCs and component manufacturers, pursuing a nuclear market entry strategy is challenging due to the potential opportunity cost of widening the focus from an already robust non-nuclear project backlogs.

The last year may eventually be looked back upon as a transition year for nuclear equipment and services suppliers, although given long lead times of projects, the data will not show an inflection point in 2025 or even the next few years. Many participants in last decade’s nuclear stall out are still nursing their wounds and thus may apply an even greater risk premium than current dynamics warrant. There is no well defined nuclear market entry strategy. Suppliers will need not only to develop strategies tailored to their products, capabilities, and risk appetite but also adopt a degree of capital planning agility and risk mitigation that likely exceeds recent, non- nuclear growth platform endeavors.

Owen Ward, President at Solestiss, has over 20 years’ experience leading go-to-market strategy and commercial execution for a range of advanced energy products and business lines, including for two Gen IV small modular reactor (SMR) developers. Prior to managing the Solestiss business and leading market advisory work, he spent ten years in the Power & Utilities team at Booz & Company / PwC Strategy& and six years at Cummins.

Kim Smiley is an Executive Consultant at Solestiss advising clients on advanced nuclear strategy, market positioning, and execution planning for complex energy initiatives. She began her career as an engineer in the U.S. Naval Nuclear Propulsion Program and brings a practical, systems-oriented perspective to helping organizations navigate first-of-a-kind projects and turn strategy into executable plans.